My town is going to make the downtown area paid parking, both on-street and parking lots.

They will have signs with a QR code to scan which takes you to a website. You enter your license # and credit card. Or the other option is to use the Flowbird app (rated 3.6/5 on the Play Store, not great).

For parking in many other places, there is often a kiosk where I can use cash or card. But my town is going to do phone only.

I don’t pay for anything over my phone – I don’t trust that the connection is secure.

I looked up online and found a few articles about the safety (or hazards) of such a method of payment.

Does anyone have knowledge or experience about this method of paying for parking?

I sometimes have to use the Park Detroit app for parking in Downtown areas. This app works with numbered parking zones, you either use a terminal in the zone to pay, or feed your car information into the app with a card payment method.

I haven’t had to use it for a few years, but the next time I do, I intend to give it a Privacy.com virtual card number with a low limit. The virtual card will lock to the merchant ID on first use. If someone can enter the card for the same parking app, a low limit can prevent too much money leakage, and they can’t use the card for anything else.

If you are worried about your vehicle information, I’m not able to address that.

I also have the ParkWhiz app, for use in private lots all around the country. I’ve used it exactly twice, in cases where I had to be where I was. Park Whiz gets me discounted parking compared to normal rates, and a guaranteed space. (Used one or more days in advance of when I am going somewhere.) Normally paid parking means a no-go zone. But there are times where I literally have no realistic choice in the matter.

I think the ease of printing a bogus QR code to place over the parking meter’s code is definitely a cause for concern. And to add insult to injury, I’d probably get a parking fine for failing to pay the legit parking fee.

I second @mwgardiner’s recommendation to use Privacy.com to spin up temporary, limited-use credit cards for this kind of situation. I’ve been a Privacy.com customer for many years and use them all the time.

I had never heard of privacy.com before either. I like that it becomes coupled to a single payee so if the number is stolen it is effectively useless unlike a regular card where you have to work through with the bank which charges are valid and which aren’t. Glad it was brought up even though I would not pay for parking via a QR code.

The thing is, there isn’t a choice on how to park, at least at my town’s location.

I was in another town where you could do the QR code, or the kiosk in the lot.

It adds another thing to know before one travels somewhere - research the parking!

If I ever end up in one of those QR-Code areas, I will photograph the QR code before using it, then if I get a ticket I have visual proof of things and might be able to escape fines for non-payment. Governments never let basic charges go unpaid, so I would have to pay a second time for parking, assuming the scammer got any money at all.

For Privacy.com cards you can set a limit for per-transaction, per-month per-year and Total for the card. In this case I would set a per-transaction limit of a little more than the expected parking charge.

Be aware that scammy businesses have figured out how to spot disposable card numbers and will refuse them. If that happens, find a way to avoid that organization. No legitimate business has a good reason to do that.

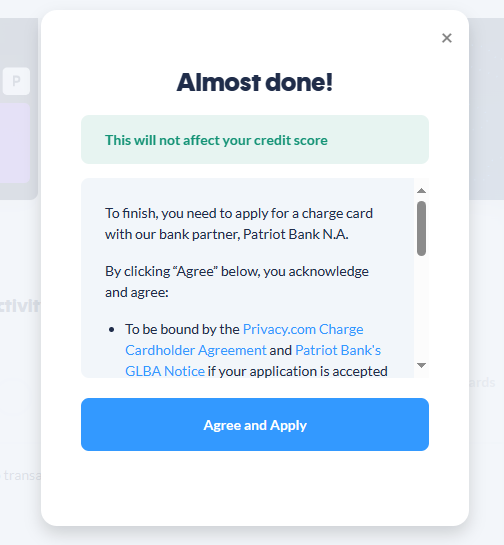

So I created an account with Privacy.com, input all of my info, and my bank info was accepted. But before I can use it, their terms require that I apply for their Patriot Bank credit card.

But nowhere in the application process did it say I would have to get a new credit card – I don’t want one, and I froze my credit bureau accounts.

For those who use Privacy.com – is this what happened to you? I just think they should disclose up front that you will have to apply for a new credit card before using privacy.com !!

I’ve been using Privacy since, if I remember correctly, 2017. There was no requirement one apply for a credit card of any type. In fact, Privacy’s whole rationale is their virtual cards are drawn from one’s associated bank account rather than any card.

I understand Patriot Bank is referenced in the Terms and Conditions to which one must agree when signing up for Privacy. Privacy does use Patriot Bank to clear transactions. Are you certain you are being asked to sign up for a credit card? If so, that would be a big change in Privacy’s practices.

For what it’s worth, this is what Privacy has to say:

Further, for what it’s worth, in going on seven years using Privacy, I’ve, literally, never had a problem with the service.

That’s why this surprised me. I can’t continue on to use Privacy.com until I agree to get their credit card. But they have my verified bank information, so I should be able to make a virtual credit card!!

The screenshot states: “To finish, you need to apply for a charge card with our bank partner, Patriot Bank N.A.”

I sent a message to them and am waiting to see what they say.

Is it the “charge card” language that is of concern to you? If so, a charge card is not the same thing as a credit card. With a charge card unlike a credit card the total balance is always due. One cannot carry a balance, there is no interest and no impact to your credit score per Privacy:

Examples of charge cards as opposed to credit cards are the original green American Express card (which Amex may or may not still issue) and many store charge cards. In other words, if one spends $50 on a charge card, the balance must be paid in full when due (with Privacy this is per transaction and debited from one’s linked bank account). With other types of charge cards, there’s typically a monthly billing date, however, unlike credit cards, one cannot make a small minimum payment while carrying a balance.

I can appreciate the concern. Colloquially, the terms credit card and charge card are used interchangeably but they are not actually the same thing.

It’s similar to calling all mobile service providers carriers. They’re not. Carriers own their telephone network. Most mobile service providers are MVNOs (mobile virtual network operators) and do not own the networks there services operate on. For example, Tello is an MVNO using T-Mobile’s network. T-Mobile not Tello is the carrier.

All cards (physical or virtual) require an issuing bank. That is the role of Patriot Bank with Privacy. Patriot is the issuing bank for Privacy virtual cards. Neither Privacy or Patriot Bank are providing credit. I say this as a former banker.

I clicked “agree” to it, and it looks like I may be ready to go!

I plan to use it for paid parking, so hopefully it will go OK.

Thanks!

Customer service did get back to me and said something similar to what Rolandh said – it’s not a credit card per se.

I guess it’s kind of like a line of credit that must be paid off.

I suggested that they explain this at the start of the account process, not present it at the end. It had me very confused!

I find I must now revoke my recommendation of Privacy.com, and change my comment to: Avoid.

Two weeks ago I got an e-mail from one of my services that my charge had been declined. I was able to switch that service to a real debit card before service was terminated. I also got a note from Privacy.com that my account has been suspended. App says they are reviewing my account. It still says suspended. Not that the outcome of the “review” means anything. On financial operations of any type, screw-ups are not tolerated. The rule is one-and-done. I’ve been reverting my charges to a real debit card as there does not seem to be anyone else competent-looking operating in that payment space.

Once I’ve finished reverting the various services, I’ll contact Privacy.com to terminate the account.

Out of curiosity, do you know if the purchase was declined due to the account suspension? Has Privacy explained the reason for the suspension and review? Have you asked?

For what it’s worth, I’ve been using Privacy for six years or so now. In that time, there hasn’t been a single hiccup. The only charges declined by Privacy were those that exceeded limits I placed on a virtual card and, without fail, Privacy itself has notified me of the declined charge giving me the opportunity to take corrective action if warranted.

They flat-out told me that that is why the charge was declined. They haven’t explained anything yet, and I will ask about it when I contact them about terminating the account.

I managed to replace all my defunct Privacy cards with a real one on all accounts.

The app has no cancel option so I went to the web site. That is when I found out they wanted to confirm my information. Instead of just sending a message asking to verify the information, they suspend the account. This is such an insanely stupid action that I must assume they are trying to chase off their customers.

On top of that, the web site eventually complained that it could not cancel my account, and to try again later. I sent an e-mail to thier support address requesting that I be cleaned out of their systems, and I explained in no uncertain terms how they had screwed up. I advise anyone using these lackwits to dump them sooner than is possible.

Yeah. If it works for you, great. I guess I just don’t get the point. My debit and credit cards all have fraud protection. They’ve all been compromised at some point. I just report it and the money gets refunded. I guess the attraction is that you don’t have to actively monitor extraneous charges. I just don’t know who the folks behind privacy.com are. I’d rather just deal with my bank directly.

My reason for going with Privacy was when a training vendor had an incident and my debit card was compromised. Contacting all those who were using that card with a new card, and I had to do it twice as the same vendor got cracked again. Having to deal with this again because of the incompetence of the company I was relying on to not have to do that again is just a whole new level of irritating.